Samsung Q2 2026 Profit Surges on AI Memory Chip Boom

Samsung Q2 2026 Profit Surges on AI Memory Chip Boom

Samsung Electronics delivered one of the most dramatic earnings surprises in its history on July 7, 2026, forecasting a nineteen-fold jump in second-quarter operating profit compared with the same period a year earlier. The preliminary Samsung Q2 2026 profit figure, estimated at 89.4 trillion won, or roughly $58.4 billion, beat analyst expectations compiled by LSEG and marked the company's third consecutive quarter of record operating profit. It is a number so large that it now exceeds Samsung's combined operating profit for the three full years from 2023 through 2025, a scale of improvement that even seasoned semiconductor analysts have described as historic.

The driver behind the Samsung Q2 2026 profit surge is straightforward in outline, even if the underlying dynamics are complex: an extraordinary, sustained boom in demand for memory chips used to power artificial intelligence infrastructure. Data center operators and hyperscale cloud providers around the world have been racing to build out the computing capacity needed to train and run increasingly capable AI models, and that buildout depends heavily on high-bandwidth memory, conventional DRAM, and NAND flash storage, the exact categories of chips where Samsung has long held a dominant global market position.

Why Samsung's Q2 2026 Profit Jumped So Sharply

To understand the scale of the Samsung Q2 2026 profit jump, it helps to look at what happened to memory chip pricing over the past several quarters. Contract prices for DRAM and NAND products climbed between roughly 40 percent and 65 percent in a single quarter, according to industry pricing data, an increase driven almost entirely by the imbalance between AI-related demand and available manufacturing capacity. Samsung has reportedly gone further still, pushing for an additional 20 percent increase in DRAM contract prices heading into the third quarter, a sign that the company believes the current supply squeeze has more room to run rather than easing in the near term.

Executives at Samsung's semiconductor division have been unusually direct in public commentary about the scale of this cycle. Kim Yong-kwan, who heads the company's Device Solutions division, told an internal all-employee meeting in early July that the division's full-year 2026 operating profit is expected to exceed the cumulative operating profit Samsung has generated across four decades in the semiconductor business. That is not a marginal claim. It implies that a single year of AI-driven memory demand is now worth more to Samsung's chip business than every year combined since the company entered the semiconductor industry.

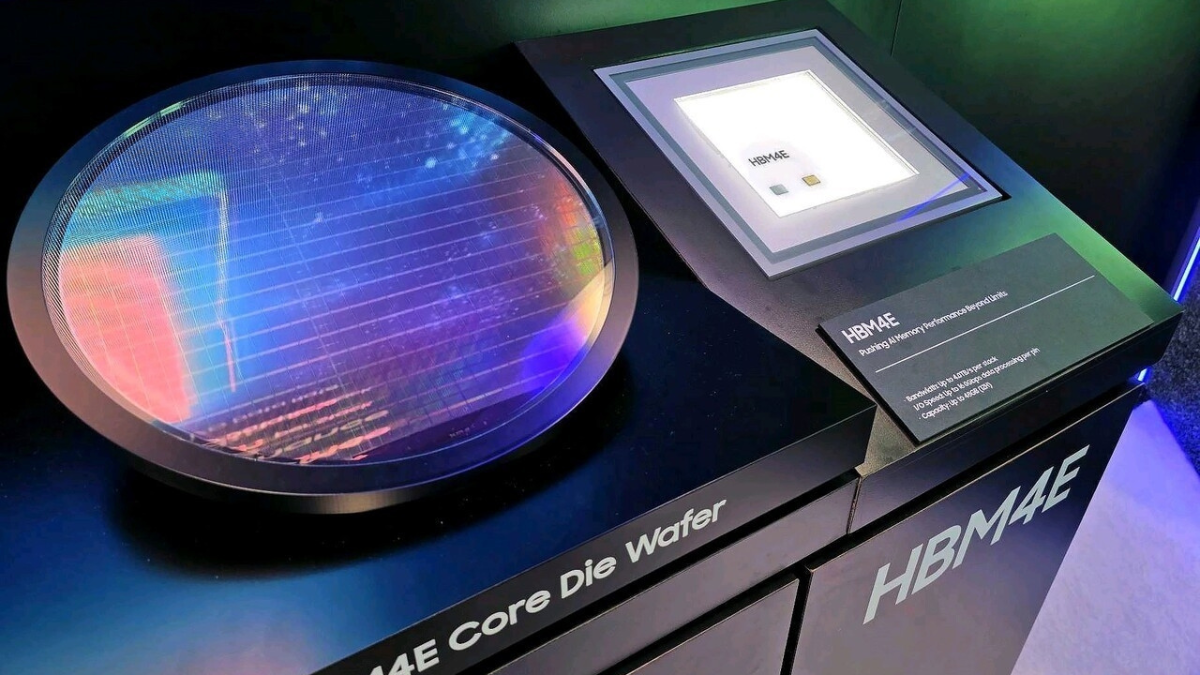

High-Bandwidth Memory and the AI Supply Chain

A central piece of the Samsung Q2 2026 profit story is high-bandwidth memory, commonly known as HBM, which sits alongside advanced processors inside the servers that power large AI models. Demand for HBM has been so strong that it accounted for the overwhelming majority of Samsung's semiconductor profit in recent quarters, with some reports indicating AI-related memory made up roughly 94 percent of total chip division profit in the most recent full quarterly disclosure. Samsung has been working to expand its share of this market and to secure formal product certifications with major AI chip designers, a process that has historically favored rival SK Hynix but which Samsung's leadership has signaled as a top strategic priority.

"In H2 2026, the Company expects server memory demand to remain strong as hyperscalers accommodate enterprises' increasing adoption of AI and LLM services," Samsung said in earnings commentary, adding that the emergence of agentic AI applications is expected to further accelerate demand for memory products.

This demand is not limited to the newest, most specialized HBM products either. Samsung's commentary and independent pricing data both point to broadening strength across conventional DRAM and NAND as well, suggesting that the AI buildout has begun spilling over into general-purpose memory markets that serve smartphones, personal computers, and traditional servers, not just dedicated AI infrastructure. That broadening is one reason analysts have been raising price targets across the memory sector, not just for the handful of companies most directly tied to specialized AI chips.

The Other Side of the Ledger

Not every part of Samsung's business is benefiting equally from this cycle, and the Samsung Q2 2026 profit picture includes some notable cross-currents. Analysts covering the company have pointed out that Samsung's foundry and system large-scale integration, or LSI, businesses are expected to post wider losses this quarter, partly because bonus expenses tied to a new wage agreement are allocated across the entire semiconductor division rather than isolated to the highly profitable memory unit. That wage deal, agreed with chip division workers in May, links employee bonuses directly to operating profit, meaning the extraordinary profit growth in memory is also translating into extraordinary bonus costs across the division.

There is also a supply chain irony worth noting. Samsung's mobile division, which relies on memory chips as a key input for its own smartphones, is absorbing higher component costs from the same price increases that are boosting the memory division's profit. Industry observers have described this as a genuine double-edged sword: the same price hike that shows up as profit on the chip division's books can show up as a cost headwind on the device division's books, since the company is effectively both the largest beneficiary of the price increases and one of the customers absorbing them.

Market Reaction and Stock Performance

Samsung shares rose more than 4 percent in Korean trading ahead of the earnings preview, touching a high near 325,000 won, as investors positioned for the scale of the profit beat that ultimately materialized. Some analysts have suggested the stock could target the 400,000 won level if the detailed results due later in July confirm strong margin quality and continued progress in HBM certification, while cautioning that a disappointing breakdown on those specific metrics, even alongside a strong headline profit number, could trigger a "sell the news" pullback given how much of the good news was already priced in ahead of the announcement.

The broader US market reaction to the Samsung Q2 2026 profit news was also notable. The preliminary earnings, released alongside news that SK Hynix had begun the formal marketing process for its own US listing, helped fuel a rally in chip and memory-related stocks on Wall Street. The Nasdaq Composite climbed more than 1 percent and the Dow Jones Industrial Average extended its run of record closes, with semiconductor names recovering from a rough stretch in late June when concerns about a supply-chain delay had briefly rattled confidence in the broader artificial intelligence trade.

What This Means for the Broader AI Trade

The Samsung Q2 2026 profit numbers matter well beyond one company's share price because memory chips sit near the foundation of the entire artificial intelligence buildout. Every additional AI data center, every new generation of large language models, and every expansion of enterprise AI adoption ultimately requires more memory capacity, and Samsung's results are effectively a real-time readout of how tight that capacity has become. Executives across the technology sector have pointed to memory availability, alongside advanced logic chip supply and data center power constraints, as one of the practical bottlenecks that could eventually slow the pace of AI infrastructure spending if it is not resolved.

For now, the direction of travel is unambiguous: prices are rising, demand is exceeding supply, and the companies that manufacture memory chips are capturing extraordinary profit as a result. Whether that dynamic proves durable depends heavily on factors outside any single company's control, including the pace of data center construction, the availability of electrical power for new facilities, and whether AI infrastructure investment continues to grow at its current rate or begins to moderate.

Samsung Versus SK Hynix: A Two-Horse Race

No discussion of the Samsung Q2 2026 profit story is complete without addressing the company's chief rival, SK Hynix, which has emerged as one of the other major beneficiaries of the AI memory boom. SK Hynix has generally been viewed by analysts as further along in securing high-bandwidth memory certifications with leading AI chip designers, a lead that has allowed it to command a larger share of the highest-margin HBM business in recent quarters even as Samsung has posted larger absolute profit figures thanks to its broader base across DRAM, NAND, and foundry operations. The timing of SK Hynix's move to begin marketing its American depositary receipts for a Nasdaq listing, arriving in the same week as Samsung's earnings preview, is widely seen as an effort to capitalize on peak investor enthusiasm for the memory sector while the AI narrative remains strong.

For investors trying to decide how to position within the memory sector, the competitive dynamic between the two Korean giants matters as much as the sector's overall growth trajectory. Samsung's scale and diversification across memory, foundry, and system semiconductor businesses provide a broader base of revenue, while SK Hynix's more concentrated focus on memory, and specifically on HBM, has historically translated into higher margins during boom periods, along with greater sensitivity to any eventual downturn. Both companies' fortunes are ultimately tied to the same underlying driver: the pace at which hyperscale cloud providers continue investing in AI infrastructure.

Risks on the Horizon

Analysts covering Samsung and the broader memory sector have flagged several risks worth watching. The most frequently cited is the possibility of a slowdown in AI infrastructure investment itself, whether due to labor shortages, power grid constraints, or local opposition to new data center construction in some markets, any of which could eventually soften demand across the entire AI hardware supply chain, memory included. Memory markets have also historically been cyclical, with periods of tight supply and high prices often followed by capacity expansion and subsequent price corrections, and some analysts have cautioned that the current boom, however extraordinary, is unlikely to be permanent in its current form.

There is also company-specific risk to weigh. Samsung's ability to convert this cycle into durable market share gains, particularly in high-bandwidth memory where it has historically trailed SK Hynix in some product certifications, remains an open question that the market will be watching closely when full segment results arrive on July 30. Success in securing high-profile AI partnerships and demonstrating improved HBM market share are widely viewed by analysts as the key catalysts that would justify further valuation expansion in Samsung shares beyond the current earnings-driven rally.

The Bigger Picture

The Samsung Q2 2026 profit surge is, in one sense, a story about a single company's extraordinary quarter. In a more important sense, it is a data point that helps investors everywhere understand just how much economic value is currently flowing through the memory chip layer of the AI supply chain. As long as demand for AI infrastructure continues to outpace the industry's ability to add manufacturing capacity, companies positioned at that supply chokepoint, Samsung foremost among them, are likely to keep capturing an outsized share of the profit pool. The detailed results due July 30 will offer the next major test of whether this cycle still has room to run.

According to Reuters, CNBC, TradingKey, KuCoin, SamMobile, and Samsung Global Newsroom.