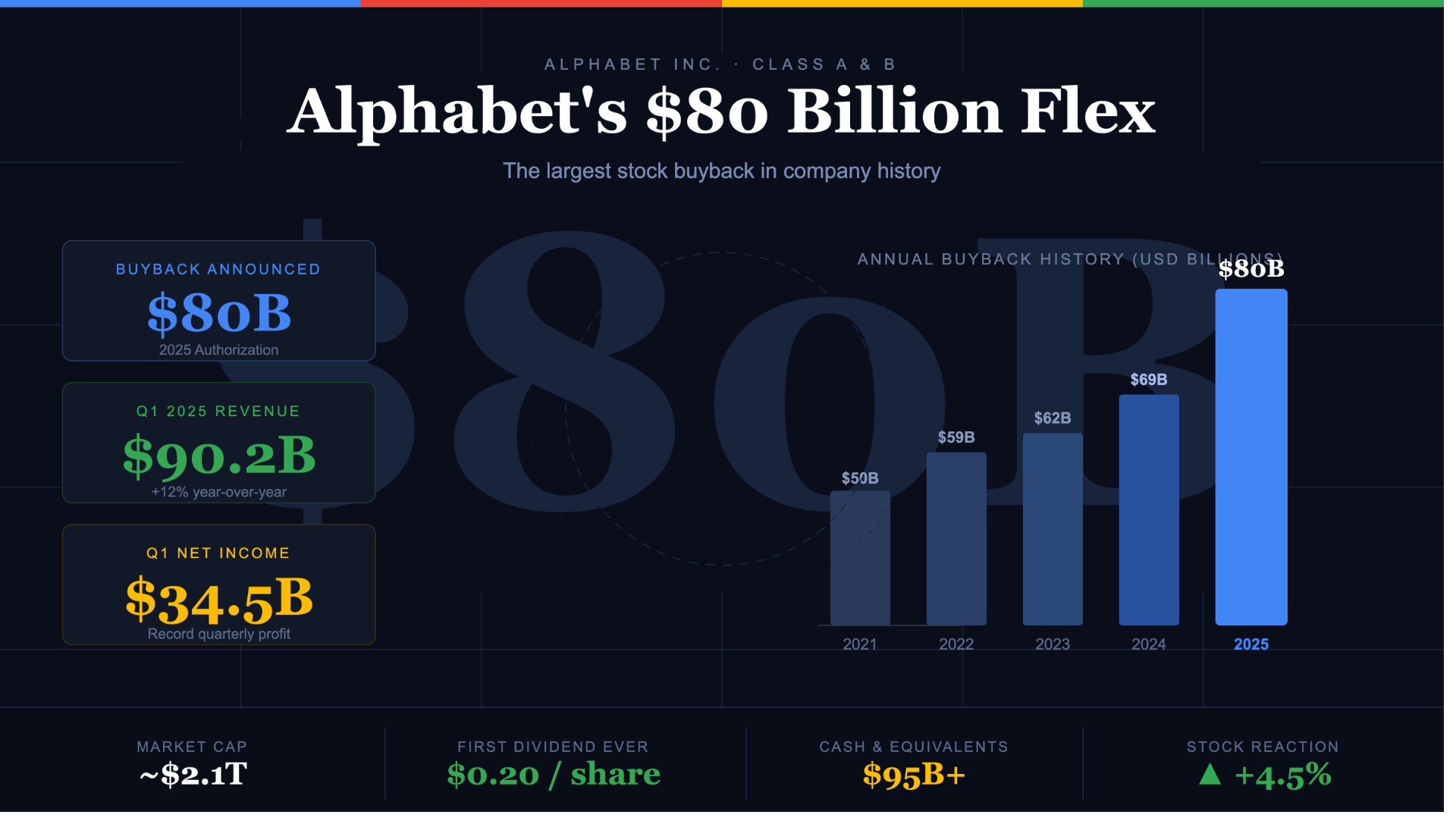

Alphabet’s $80B Flex Reshaping Tech Markets

The current wave of artificial intelligence infrastructure spending has created one of the most unusual market environments in recent memory. What began as a supply-constrained semiconductor cycle has evolved into something far more aggressive: a full-scale, hyperscaler-driven buildout of global compute capacity. At the center of this transformation sits what many analysts now loosely describe as Alphabet’s $80 Billion Flex, a shorthand for Alphabet’s escalating capital expenditure strategy and its broader implications for the entire AI supply chain.

According to commentary featured in The Motley Fool, the scale of hyperscaler spending is no longer incremental. It is exponential, with Alphabet, Meta, Microsoft, and Amazon repeatedly revising capital expenditure upward. In this environment, Alphabet’s $80 Billion Flex is not just a corporate spending figure—it is a signal that demand for compute infrastructure is outrunning even the most aggressive forecasts.

This article explores how this dynamic is reshaping the market for hardware suppliers like Dell and HP Enterprise, why memory and GPU cycles are becoming increasingly distorted, and why investors are struggling to reconcile strong earnings with rising uncertainty.

The Compute Tsunami and Market Repricing

The most striking feature of the current cycle is not just demand growth—it is the lack of normalization. Traditionally, hardware cycles move from shortage to equilibrium to oversupply. This time, however, the industry appears stuck in a prolonged shortage phase.

As one commentator described in the referenced Motley Fool Hidden Gems Investing discussion, this is not a tide lifting all boats. It is closer to a “tsunami” lifting the entire infrastructure stack by an unnatural magnitude. That framing captures the essence of Alphabet’s $80 Billion Flex: hyperscalers are not merely investing in growth, they are aggressively securing capacity far ahead of demand curves.

What makes this cycle distinct is the nature of procurement behavior. Instead of optimizing for efficiency or best-in-class technology, companies are prioritizing availability. Compute is being sourced from multiple vendors, including lower-tier hardware, simply to ensure capacity is physically deployed. This has created a distorted pricing environment where scarcity outweighs performance differentiation.

Alphabet’s $80 Billion Flex becomes a symbol of this distortion. Alphabet’s broader capex trajectory—alongside Meta and others—is driving a secondary wave of demand that cascades through every layer of the supply chain, from GPUs to servers to networking equipment.

Hyperscaler Capex Explosion and the Illusion of Predictability

The hyperscaler investment cycle is increasingly difficult to model. Alphabet alone has been associated with capital expenditure guidance in the range of $180–200 billion annually, according to analysts cited by The Motley Fool. Meta, meanwhile, has explored off-balance-sheet structures to expand infrastructure spending flexibility.

Within this environment, Alphabet’s $80 Billion Flex represents a microcosm of a broader phenomenon: sustained upward revisions in capital intensity assumptions. Each earnings cycle brings higher guidance, not lower, which contradicts typical infrastructure normalization expectations.

The challenge for investors is that these spending commitments are forward-loaded and multi-year in nature. Once contracts are signed and infrastructure is planned, hyperscalers are effectively locked into procurement pipelines that extend years into the future. This creates a feedback loop where demand visibility itself drives further supply investment.

Alphabet’s $80 Billion Flex therefore functions less as a single data point and more as a directional indicator of structural demand. The assumption underpinning many valuations is that hyperscaler spending will remain elevated through the end of the decade. If that assumption weakens, the entire supply chain valuation framework could shift rapidly.

Dell, HP Enterprise, and the Revival of “Old Tech”

One of the most surprising outcomes of the AI infrastructure boom has been the resurgence of legacy enterprise hardware companies. Dell and HP Enterprise—companies often viewed as mature or cyclical—have become some of the market’s strongest performers.

This resurgence is directly tied to the physical reality of AI deployment. While software narratives dominate headlines, AI workloads still require servers, racks, cooling systems, and networking hardware. As Alphabet’s $80 Billion Flex continues to pull demand forward, these companies sit in a critical bottleneck position.

Travis Hoium’s observation in the Motley Fool Hidden Gems Investing discussion highlights this shift: the industry is no longer optimizing for elegance but for throughput. “Grab every spare part and slap it together,” as one participant described it, reflects a procurement environment where speed of deployment outweighs architectural perfection.

In this context, Dell and HP Enterprise are not just beneficiaries—they are infrastructure enablers. Their order books reflect hyperscaler urgency, not traditional enterprise refresh cycles. Alphabet’s $80 Billion Flex amplifies this effect by anchoring expectations of sustained demand rather than cyclical spikes.

Semiconductors, Memory, and the Return of Volatility

The semiconductor sector, particularly memory manufacturers like Micron, has historically been one of the clearest indicators of cyclical demand shifts. Yet even this signal has become distorted.

Lou Whiteman’s commentary points to an unusual market behavior: attention rotates away from traditional bellwethers like Micron and toward infrastructure integrators like HP Enterprise. This suggests that investors are struggling to interpret where value is actually being created in the stack.

Within this environment, Alphabet’s $80 Billion Flex adds upward pressure on every component of compute infrastructure. GPUs from Nvidia remain highly constrained, while memory supply fluctuates in response to unpredictable demand surges from AI training clusters.

The result is a fragmented supply chain where pricing power shifts rapidly between segments. Nvidia may command premium margins in GPU design, while memory manufacturers experience lagged cycles, and server OEMs benefit from assembly bottlenecks.

According to The Motley Fool, the current cycle resembles a post-disaster reconstruction phase rather than a traditional growth phase. In such environments, pricing becomes less about efficiency and more about availability. Alphabet’s $80 Billion Flex sits at the center of this dynamic imbalance.

The ROI Paradox and Corporate Uncertainty

Perhaps the most important tension in the market today is not supply, but return on investment. Corporate buyers of AI infrastructure are beginning to ask harder questions about monetization and efficiency.

Travis Hoium highlighted an important contradiction: hyperscalers continue to expand spending aggressively, yet enterprise customers are increasingly focused on measurable ROI from AI deployments. These two forces are moving in opposite directions.

Alphabet’s $80 Billion Flex symbolizes this paradox. On one hand, Alphabet and peers are accelerating infrastructure investment. On the other hand, downstream users are beginning to slow experimentation and demand clearer productivity gains before scaling further.

If hyperscalers continue spending aggressively while enterprise adoption slows, the system enters a mismatch phase where supply growth outpaces monetization capacity.

This mismatch raises fundamental questions about sustainability. Can cloud providers maintain pricing power if customers demand ROI discipline? Or does infrastructure expansion inevitably compress margins over time?

Alphabet’s $80 Billion Flex does not resolve this tension—it intensifies it.

Market Cycles, Memory Effects, and the Risk of Overextension

Historically, infrastructure booms tend to overshoot. The telecom buildout of the early 2000s and the cloud expansion of the 2010s both followed similar patterns: rapid capex acceleration followed by eventual normalization and margin compression.

What makes the current cycle different is its foundation in artificial intelligence, a technology whose long-term demand profile remains uncertain but potentially enormous. This ambiguity complicates traditional cycle analysis.

Alphabet’s $80 Billion Flex sits at the center of this ambiguity. It reflects both genuine structural demand for compute and speculative forward investment in an uncertain future.

If demand for AI workloads continues to grow exponentially, today’s infrastructure buildout may appear conservative in hindsight. However, if monetization lags persist, the industry could face a period of asset underutilization and pricing pressure.

Investors are therefore caught between two narratives: one of sustained scarcity and one of eventual oversupply. Neither can be fully dismissed.

What Investors Should Watch Next

The next phase of the AI infrastructure cycle will likely be defined by three key variables: capital expenditure trajectories, enterprise AI adoption rates, and supply chain normalization.

Alphabet’s $80 Billion Flex remains a central reference point for all three. If Alphabet and its peers continue raising capex guidance, it signals sustained scarcity. If they stabilize or reduce spending, it may indicate approaching equilibrium.

- Hyperscaler Capex Guidance: Watch for continued upward revisions from Alphabet, Meta, and Microsoft.

- Hardware Supply Signals: Monitor Dell, HP Enterprise, Nvidia, and Micron for backlog stability and pricing trends.

- Enterprise ROI Metrics: Evaluate whether AI deployments are translating into measurable productivity gains.

According to The Motley Fool, the current environment is defined by uncertainty rather than clarity. That uncertainty is precisely what makes Alphabet’s $80 Billion Flex such a critical marker for investors trying to understand the durability of this cycle.

Ultimately, the question is not whether demand exists today, but whether it will persist at a scale that justifies the infrastructure being built. Until that is resolved, the market remains suspended between expansion and skepticism, with Alphabet’s $80 Billion Flex acting as both catalyst and question mark.